Geneva – The International Air Transport Association (IATA) released

data for global air cargo markets showing slower growth in November

2021. Supply chain disruptions and capacity constraints impacted demand,

despite economic conditions remaining favorable for the sector.

As comparisons between 2021 and 2020 monthly results are

distorted by the extraordinary impact of COVID-19, unless otherwise

noted, all comparisons below are to November 2019 which followed a

normal demand pattern.

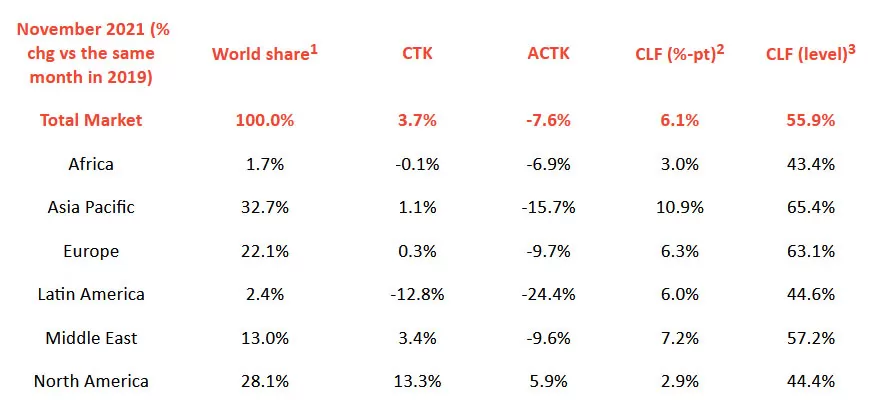

- Global demand, measured in cargo tonne-kilometres (CTKs*), was

up 3.7% compared to November 2019 (4.2% for international operations).

This was significantly lower than the 8.2% growth seen in October 2021

(9.2% for international operations) and in previous months.

- Capacity was 7.6% below November 2019 (-7.9% for international

operations). This was relatively unchanged from October. Capacity

remains constrained with bottlenecks at key hubs.

- Economic conditions continue to support air cargo growth,

however supply chain disruptions are slowing growth. Several factors

should be noted:

- Labor shortages, partly due to employees being in quarantine,

insufficient storage space at some airports and processing backlogs

exacerbated by the year end rush created supply chain disruptions.

Several key airports, including New York’s JFK, Los Angeles and

Amsterdam Schiphol reported congestion.

- Retail sales in the US and China remain strong. In the US

retail sales were 23.5% above November 2019 levels. And in China online

sales for Singles’ Day were 60.8% above their 2019 levels.

- Global goods trade rose 4.6% in October (latest month of data),

compared to pre-crisis levels, the best rate of growth since June.

Global industrial production was up 2.9% over the same period.

- The inventory-to-sales ratio remains low. This is positive for

air cargo as manufacturers turn to air cargo to rapidly meet demand.

- The recent surge in COVID-19 cases in many advanced economies

has created strong demand for PPE shipments, which are usually carried

by air.

- The November global Supplier Delivery Time Purchasing Managers Index (PMI) was at 36.4. While values below 50 are normally favorable for air cargo, in current conditions it points to delivery times lengthening because of supply bottlenecks.

- Labor shortages, partly due to employees being in quarantine,

insufficient storage space at some airports and processing backlogs

exacerbated by the year end rush created supply chain disruptions.

Several key airports, including New York’s JFK, Los Angeles and

Amsterdam Schiphol reported congestion.

“Air cargo growth was halved in November compared to October because

of supply chain disruptions. All economic indicators pointed towards

continued strong demand, but the pressures of labor shortages and

constraints across the logistics system unexpectedly resulted in lost

growth opportunities. Manufacturers, for example, were unable to get

vital goods to where they were needed, including PPE. Governments must

act quickly to relieve pressure on global supply chains before it

permanently dents the shape of the economic recovery from COVID-19,”

said Willie Walsh, IATA’s Director General.

To relieve supply chain disruptions in the air cargo industry, IATA is calling on governments to:

- Ensure that air crew operations are not hindered by COVID-19 restrictions designed for air travelers.

- Implement the commitments governments made at the ICAO High

Level Conference on COVID-19 to restore international connectivity,

including for passenger travel. This will ramp-up vital cargo capacity

with “belly” space.

- Provide innovative policy incentives to address labor shortages where they exist.

- Support the World Health Organization / International Labour Organization Action Group being formed to assure freedom of movement for international transport workers.

1 % of industry CTKs in 2020 2 Change in load factor vs 2019 3 Load factor level

- Asia-Pacific airlines saw their international air cargo volumes increase 5.2% in November 2021 compared to the same month in 2019. This was only slightly below the previous month’s 5.9% expansion. International capacity in the region eased slightly in November, down 9.5% compared to 2019.

- North American carriers posted an 11.4% increase in international cargo volumes in November 2021 compared to November 2019. This was significantly below October’s performance (20.3%). Supply chain congestion at several key US cargo hubs has affected growth. International capacity was down 0.1% compared to November 2019.

- European carriers saw a 0.3% increase in international cargo volumes in November 2021 compared to the same month in 2019, but this was a significant drop in performance compared to October 2021 (7.1%). European carriers have been affected by supply chain congestion and localized capacity constraints. International capacity was down 9.9% in November 2021 compared to pre-crisis levels and capacity on the key Europe-Asia route was down 7.3% during the same period.

- Middle Eastern carriers experienced a 3.4% increase in international cargo volumes in November 2021, a significant drop in performance compared to the previous month (9.7%). This was due to a deterioration in traffic on several key routes such as Middle East-Asia, and Middle East-North America. International capacity was down 9.7% compared to November 2019, a small decrease compared to the previous month (8.4%).

- Latin American carriers reported a decline of 13.6% in international cargo volumes in November compared to the 2019 period. This was the weakest performance of all regions and a significant deterioration from the previous month’s performance (-5.6%). Capacity in November was down 20.1% on pre-crisis levels.

- African airlines’ saw international cargo volumes increase by 0.8% in November, a significant deterioration from the previous month (9.8%). International capacity was 5.2% lower than pre-crisis levels.

Be the first to comment on "Supply Chain Disruptions Halve November Air Cargo Growth"