easyJet Trading Update for the Six Months ending 31 March 2020

easyJet expects to deliver a first half headline loss before tax in the range of £185m to £205m, representing an improved year-on-year first half headline loss before tax (H1 2019: £275m).

Decisive cost actions, deferring the purchase of 24 new aircraft and the raising of significant new finance ensure that easyJet has sufficient liquidity to endure a lengthy fleet grounding.

Johan Lundgren, easyJet CEO said: “Our first half trading performance was very strong prior to the impact of coronavirus, which shows the strength of easyJet’s business model.

“Since then I have been immensely proud of our team, right across the business, and the way they have worked through these tough times to put us in the strong position we are in now. We took swift action to meet the challenges of the virus and in a period of around 7 weeks have:

• Launched a cost cutting initiative and dramatically brought down our cash burn

• Grounded our entire fleet in a well planned and executed process

• Delivered an updated fleet deal deferring 24 aircraft, while also maintaining a level of flexibility that will be very important when this crisis ends

This change, combined with the deferral and cancellation of a number of other projects has helped to drive a circa £1 billion decrease in capex over three years: and finally

• Executed a funding programme which will add almost £2 billion in extra cash funding, strengthening our liquidity position.

“These decisive actions mean that easyJet is well positioned to endure a prolonged grounding.

“We remain focused on doing what is right for the company for its long term health and to ensure we are in a good position to resume flying when the pandemic is over.

While the vast majority of our people are not able to work at this time, there is a small number working tirelessly to help our customers, and to plan for our return to the skies, whenever that might be”.

Revenue

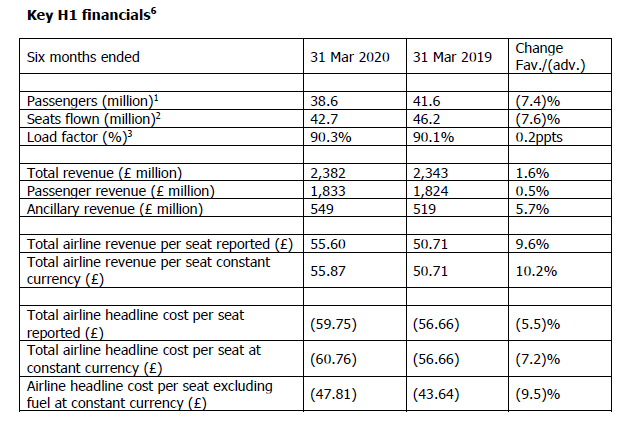

Total revenue for the six months ending 31 March 2020 increased by 1.6% to £2,382 million

(H1 2019: £2,343m), with seat capacity2 decreasing by 7.6% to 42.7 million (H1 2019:46.2m).

Airline revenue per seat at constant currency is expected to have increased by 10.2%. This reflects a continuation of the strong performance seen in Q1, with a very strong RPS performance in January and February, prior to the impact of the travel restrictions caused by coronavirus.

easyJet’s fleet was fully grounded on 30 March 2020. Our winter 20/21 seats were released earlier than usual, in order to allow customers to plan ahead. Bookings for winter are well ahead of the equivalent point last year, and this includes customers who are rebooking coronavirus-disrupted flights for later dates.

During the coronavirus pandemic we are providing customers with the options of changing their flights (with no change fee), receiving a voucher for the value of the booking or receiving a refund. Since we introduced the online voucher option, more than half of disrupted passengers have chosen vouchers or alternative flights.

At this stage there can be no certainty of the date for restarting commercial flights. We will evaluate continuously based on changing regulations and customer demand and will update the market in due course. Our strategy, network and data science teams are working

through different demand scenarios for re-starting flying, which could be done with as little as two weeks’ notice.

Operating costs

Total headline cost in the first half is expected to decrease by 1.6% as a result of reductions in variable expenses such as fuel and airport charges. Airline headline cost per seat excluding fuel at constant currency is expected to have increased by 9.5% during the first half.

The underlying cost per seat ex fuel at constant currency increase of c.5% is in line with the guidance given in January for ‘mid-single digit’ increases in cost per seat at constant currency excluding fuel.

This increase was driven by:

o Lower capacity growth for the half;

o Ongoing regulatory and inflationary pressure in our airport charges and ground handling, as well as the expected one-off maintenance charge which we discussed atQ1 results;

o Ownership costs; and

o Crew pay agreements and higher retention levels.

The impact of coronavirus drove a further 4.5% increase in costs, due to:

o Significant increases in disruption costs;

o Full pilot and crew rosters through much of March when many flights were being cancelled, with furlough leave only starting after the end of H1; and

o Significantly lower seat capacity.

These cost increases were somewhat offset by:

o Fall in navigation rates;

o Lower marketing expenditure;

o Reduced airport charges; and

o Wet leasing costs.

We have taken decisive action in order to remove cost and non-critical expenditure from the business at every level, to help mitigate the impact from the coronavirus. The grounding of aircraft removes significant cost.

Cost items which have changed materially include:

o Fuel – easyJet does not operate ‘take or pay’ contracts for fuel. Our fuel tenders are based on indicative volumes only. If/when we do not lift the volume of fuel we have tendered for, we are not liable. (See comments below regarding fuel hedging)

o Airports & ground handling – our teams moved quickly to reduce costs. We are currently incurring virtually no charges whilst the fleet is grounded

o People – the majority of staff across easyJet are on furlough during April and May, with a small number of skeleton staff still working in central functions. All of our base countries are offering some form of government support during the crisis.

easyJet has reached agreement in the UK with unions Unite and BALPA regarding furlough arrangements for crew and pilots and has worked with unions and works councils in all countries

o Navigation – payment terms have been extended

o Maintenance – all non-critical maintenance work has been postponed

o Selling & marketing – we are currently incurring no advertising/marketing costs.

Costs will likely be incurred once again as we enter the recovery period.

Whilst we have also undertaken cost cutting measures within easyJet holidays, it already had a high proportion of variable costs, which means that the easyJet holidays business model is low risk, with no inventory risk.

Cash flow deferrals have also been achieved through payment term extensions negotiated with many of our major suppliers including airports, ground handlers and fuel providers. All government tax payment schemes have been explored including ‘time to pay’ arrangements and reclaiming corporation tax payment on account. We estimate that our operating costs burn is in the region of £30-40 million per week, whilst the fleet is grounded. This compares to circa £125 million when flying a full schedule.

Capital costs

On 9 April easyJet announced that it had reached agreement with Airbus for the net deferral of 24 aircraft deliveries from Financial Years 2020, 2021 and 2022. This will mean that versus our previously disclosed fleet plan the following aircraft deliveries will be deferred:

o 10 aircraft deliveries in FY20

o 12 aircraft deliveries in FY21

o 2 aircraft deliveries in FY22

As a result easyJet will take no aircraft deliveries in FY21 and retains the option to defer a further 5 deliveries in FY22. Exact dates of future deliveries of the deferred aircraft are to be agreed in response to the demand environment.

easyJet’s base fleet plan for year-end September 2020 is 335 aircraft.

- Assumes the sale of 6 old aircraft yet to be transacted.

** 6 aircraft deliveries expected for the remainder of 2020. This would lead to a total of 14 deliveries for the year

We have also deferred or cancelled a number of other projects. - These measures combined have enabled us to reduce our projected capex spend by c.£1bn over three years.

Within the next 16 months easyJet also has 24 operating leases due for renewal, providing us with further flexibility, which could include deferral and cancellation.

As a result of these actions the fleet has the potential to be substantially lower than our previous plan, whilst also retaining the flexibility to respond to future demand environments. - Funding easyJet announces today that it has signed two term loans totalling c.£400m. Both loans mature in 2022 and are secured against aircraft assets.

As announced earlier this month, easyJet has successfully issued £600m of Commercial Paper through the Covid Corporate Financing Facility (CCFF). This is unsecured, short term

paper, at attractive rates. easyJet has also fully drawn down on its $500m Revolving Credit Facility, secured against aircraft assets. As a result of these two measures easyJet has already raised c.£1.0bn of cash.

Furthermore we continue to engage with an active lessor market interested in acquiring aircraft from easyJet’s fleet on a sale and leaseback basis. Announcements on the progress of these engagements will be made in due course, with anticipated proceeds expected to be in the range of £400-£550m.

Following these additional funding measures, circa 50% of our fleet will remain unencumbered.

Upon closure of all these funding initiatives, we expect to have generated total additional liquidity of c.£1.85-£1.95bn leading to a notional cash balance of circa £3.3bn.

We have run scenario analysis assuming that our fleet remains fully grounded for 3 months, 6 months and 9 months, using the following assumptions:

o The ratio of passengers who choose a refund versus a non-cash alternative, namely a voucher or a later-dated flight, continues at a similar rate to our recent experience

o Our staff remain on furlough leave until the end of May

o No material change to card acquirer arrangements

o No material changes in FX or fuel rates

o Revenue from new bookings remains minimal

This analysis has shown that we have sufficient cash reserves to remain liquid across a number of scenarios:

o During a 3-month grounding easyJet would use around £1.2bn in cash;

o During a 6-month grounding we would use around £2.2bn in cash;

o During a 9-month grounding we would use around £3.0bn in cash.

Given the possibility of a prolonged grounding easyJet will continue to consider further liquidity and funding options

During a prolonged grounding there would be opportunities to further defer maintenance spending. Additional government support could be sought, around extended furlough leave

and tax relief. Further operational and organisational changes could be made.

Fuel & FX

Due to the full grounding of the fleet and the lower capacity expected for several months thereafter, easyJet is in a significantly over-hedged position from both a jet fuel and FX

perspective. This will have an adverse effect on easyJet’s income statement in the first half, due to the recording of hedge accounting ineffectiveness. In addition, with the precise

phasing of future capex deliveries yet to be agreed, we will look to hedge these future capex deliveries once we have further clarity on the position.

To mitigate the effects of over-hedging, a number of actions have been taken including the ceasing of jet fuel hedging, whilst the fleet is fully grounded, for time periods from April 2020 through to October 2021. Hedging continues for later time periods, to take advantageof the low-price environment. Once there is further clarity on the likely duration of the fleet grounding, easyJet’s regular hedging programme will resume for both FX and jet fuel.

Non-headline items

Non headline items for H1 are anticipated to include a £175m to £185m loss in relation to the over-hedging of fuel and FX4, as discussed above. This will be subject to review by our

auditors.

Customer and operational performance

On-Time Performance (OTP) was 82%. Our Customer Satisfaction (CSAT) score of 76.8% reflected extraordinary levels of incoming customer enquiries at our call centres, starting with the severe disruption to Italian flying in February and building towards the full grounding of the fleet at the end of March. Furthermore a number of our call centres had to be temporarily closed due to social distancing rules.

Traffic statistics

Load factor3 in Q2 2020 was 89.0 although we experienced a high proportion of no-shows from February onwards.

General Meeting

As previously announced, the Board has confirmed that it will call a General Meeting requisitioned by easyGroup through UBS Private Banking Nominees Limited and Vidacos Nominees Limited and will do so within the statutory requirements. Further announcements and information relating to this General Meeting will be made in due course.

Outlook

At this stage, given the level of continued uncertainty, it is not possible to provide financial guidance for the remainder of the FY20 financial year. However we continue to take every

step necessary to reduce cost, conserve cash burn, enhance liquidity, protect the business and ensure it is best positioned for a return to flying.

The first half headline loss before tax is expected to be in the range of £185m to £205m6.

The first half reported loss before tax is expected to be in the range of £360m to £380m, including the impact of £175m-185m in relation to the over-hedging of fuel and FX6.

Following the FCA’s recent update on reporting guidelines, easyJet will release half year results (for the six months to 31 March 2020) on 30 June 2020.

A copy of this Trading Statement is available at https://corporate.easyjet.com/investors

- Represents the number of earned seats flown. Earned seats include seats that are flown whether or not the passenger turns up as easyJet is a no-refund airline, and once a flight has departed a no-show customer is generally not entitled to change

flights or seek a refund. Earned seats also include seats provided for promotional purposes and to staff for business travel. - Capacity based on actual number of seats flown.

- Represents the number of passengers as a proportion of the number of seats available for passengers. No weighting of the load factor is carried out to recognise the effect of varying flight (or ‘sector’) lengths.

- Based on fuel spot price of $370pmt. US $ to £ sterling 1.22, Euro to £ sterling 1.13.

- The information relating to the term loans amounting to c£400m contained under the ‘Funding’ heading above is considered inside information. For the purposes of MAR,the person responsible for arranging the release of this announcement is Maaike de Bie, Company Secretary.

- All preliminary H1 2020 numbers subject to auditor review

Source: Easyjet

Be the first to comment on "easyjet in a good position"