ARLINGTON, Va., Jan. 31, 2024 /PRNewswire/ —

Fourth Quarter 2023

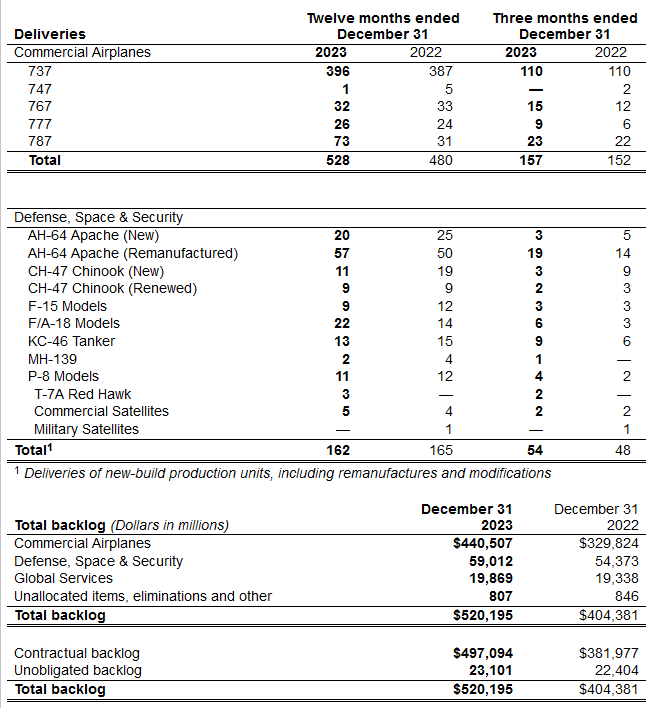

- Delivered 157 commercial airplanes and recorded 611 net orders

- 787 production rate at five per month; 737 production rate at 38 per month

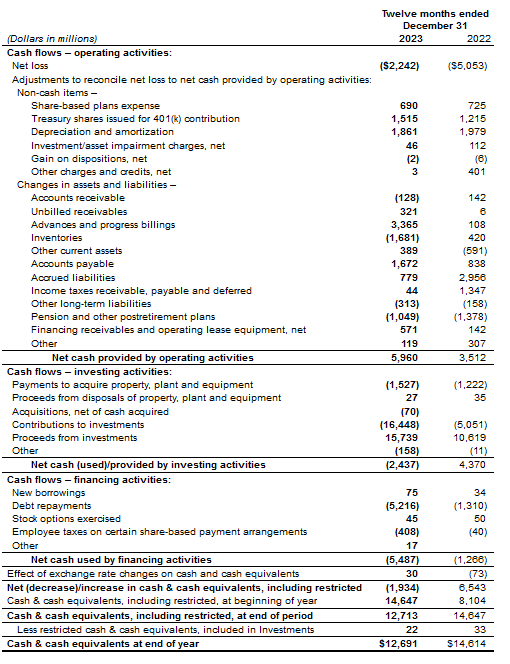

- Generated $3.4 billion of operating cash flow and $3.0 billion of free cash flow (non-GAAP)

Full Year 2023

- Delivered 528 commercial airplanes and recorded 1,576 net orders

- Total company backlog grew to $520 billion, including over 5,600 commercial airplanes

- Generated $6.0 billion of operating cash flow and $4.4 billion of free cash flow (non-GAAP)

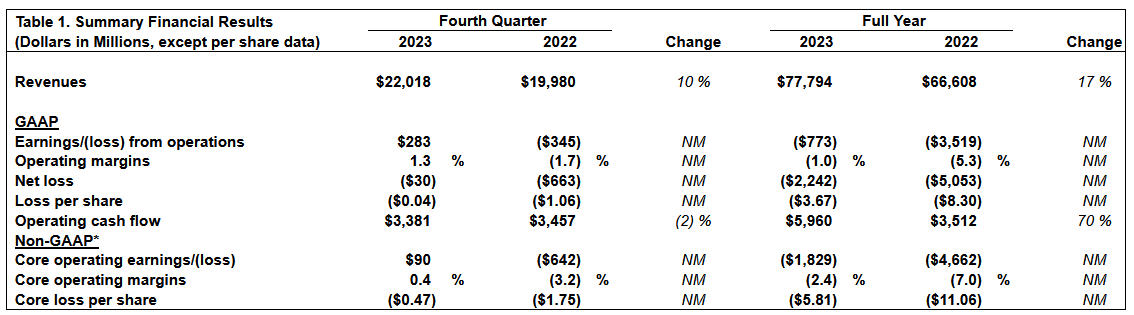

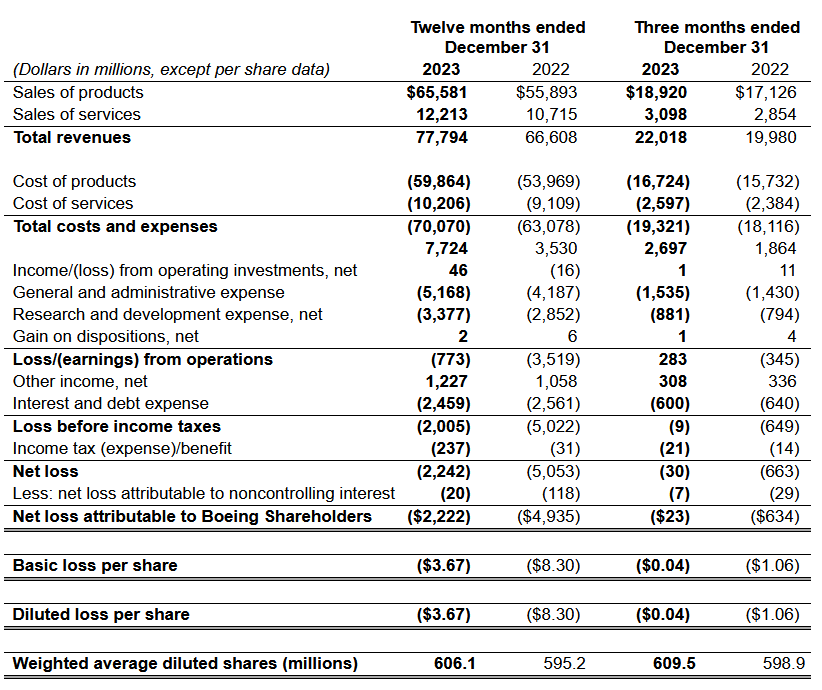

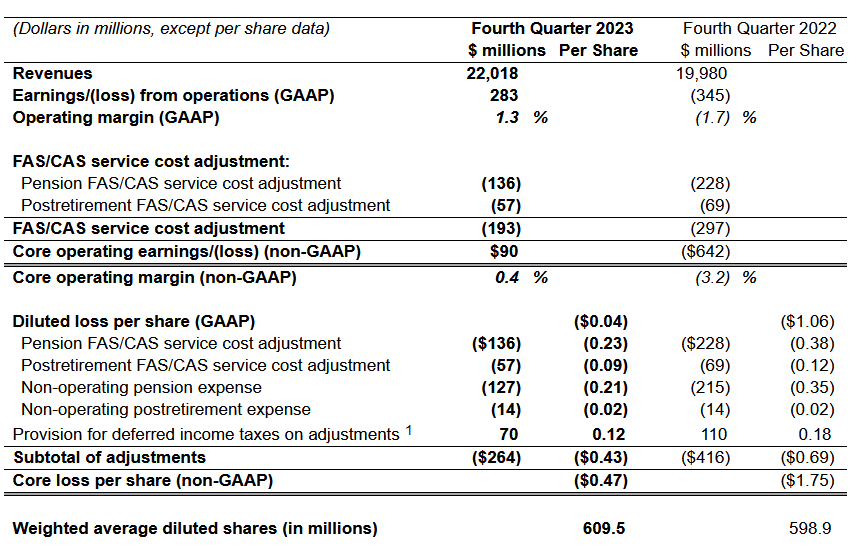

The Boeing Company [NYSE: BA] recorded fourth quarter revenue of $22.0 billion, GAAP loss per share of ($0.04) and core loss per share (non-GAAP)* of ($0.47) (Table 1). Boeing reported operating cash flow of $3.4 billion and free cash flow of $3.0 billion (non-GAAP). Results improved on higher commercial volume and performance.

“While we report our financial results today, our full focus is on taking comprehensive actions to strengthen quality at Boeing, including listening to input from our 737 employees that do this work every day,” said Dave Calhoun, Boeing president and chief executive officer. “As we move forward, we will support our customers, work transparently with our regulator and ensure we complete all actions to earn the confidence of our stakeholders.”

Operating cash flow was $3.4 billion in the quarter reflecting higher volume and favorable receipt timing (Table 2).

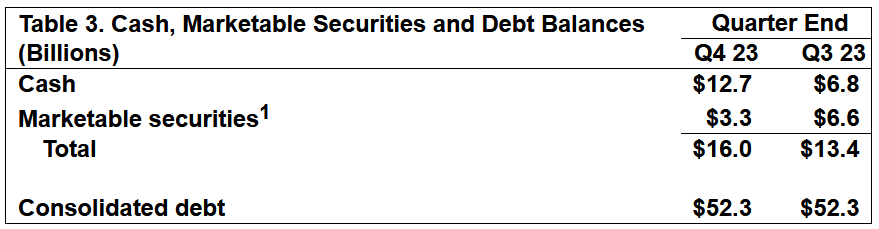

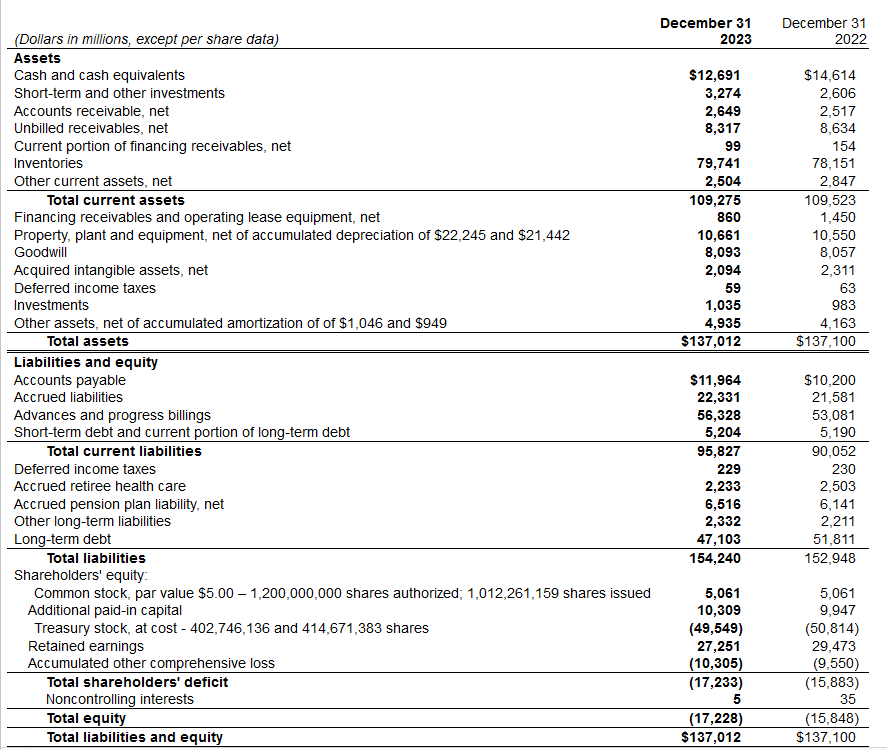

Cash and investments in marketable securities totaled $16.0 billion, compared to $13.4 billion at the beginning of the quarter (Table 3). The company has access to credit facilities of $10.0 billion, which remain undrawn.

Total company backlog at quarter end was $520 billion.

Segment Results

Commercial Airplanes

Commercial Airplanes fourth quarter revenue increased to $10.5 billion driven by higher deliveries and favorable mix (Table 4). Operating margin of 0.4 percent also reflects improved performance and lower abnormal costs.

The company continues to cooperate transparently with the FAA following the Alaska Airlines Flight 1282 accident involving a 737-9. Commercial Airplanes is taking immediate actions to strengthen quality on the 737 program, including requiring additional inspections within its factory and at key suppliers, supporting expanded oversight from airline customers and pausing 737 production for one day to refocus its employees on quality. The company has also appointed an outside expert to lead an in-depth independent assessment of Commercial Airplanes’ quality management system, with recommendations provided directly to Calhoun and the Aerospace Safety Committee of Boeing’s Board of Directors.

The 737 program continues to deliver airplanes and its production rate is now at 38 per month. The 787 program production rate is now at five per month.

During the quarter, Commercial Airplanes booked 611 net orders, including 411 737, 98 777X, and 83 787 airplanes, began certification flight testing on the 737-10, and resumed production on the 777X program. Commercial Airplanes delivered 157 airplanes during the quarter and backlog included over 5,600 airplanes valued at $441 billion.

Defense, Space & Security

Defense, Space & Security fourth quarter revenue was $6.7 billion. Fourth quarter operating margin was (1.5) percent, primarily driven by $139 million of losses on certain fixed-price development programs. Results were also impacted by unfavorable performance and mix on other programs.

During the quarter, Defense, Space & Security captured an award from the U.S. Air Force for 15 KC-46A Tankers, began the U.S. Air Force developmental flight test program for the T-7A Red Hawk, and Canada selected the P-8A Poseidon as its multi-mission aircraft. Backlog at Defense, Space & Security was $59 billion, of which 29 percent represents orders from customers outside the U.S.

Global Services

Global Services fourth quarter revenue of $4.8 billion and operating margin of 17.4 percent reflect higher commercial volume and mix.

During the quarter, Global Services opened its first parts distribution center in India and received a follow-on contract option to provide sustainment for the C-17 Globemaster III.

Additional Financial Information

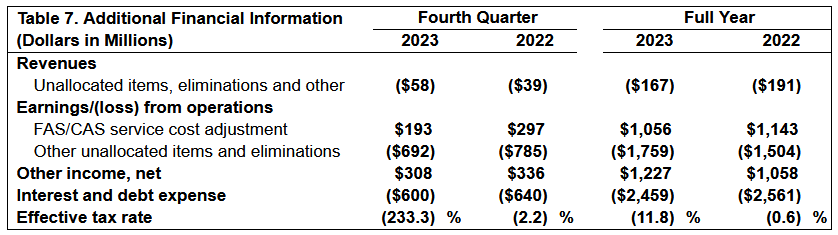

Other unallocated items and eliminations primarily reflects timing of allocations. The fourth quarter effective tax rate primarily reflects tax expense on pre-tax losses driven by an increase in the valuation allowance.

Non-GAAP Measures Disclosures

We supplement the reporting of our financial information determined under Generally Accepted Accounting Principles in the United States of America (GAAP) with certain non-GAAP financial information. The non-GAAP financial information presented excludes certain significant items that may not be indicative of, or are unrelated to, results from our ongoing business operations. We believe that these non-GAAP measures provide investors with additional insight into the company’s ongoing business performance. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently. We encourage investors to review our financial statements and publicly-filed reports in their entirety and not to rely on any single financial measure. The following definitions are provided:

Core Operating Earnings/(loss), Core Operating Margin and Core Earnings/(loss) Per Share

Core operating earnings/(loss) is defined as GAAP Earnings/(loss) from operations excluding the FAS/CAS service cost adjustment. The FAS/CAS service cost adjustment represents the difference between the Financial Accounting Standards (FAS) pension and postretirement service costs calculated under GAAP and costs allocated to the business segments. Core operating margin is defined as Core operating earnings/(loss) expressed as a percentage of revenue. Core earnings/(loss) per share is defined as GAAP Diluted earnings/(loss) per share excluding the net earnings/(loss) per share impact of the FAS/CAS service cost adjustment and Non-operating pension and postretirement expenses. Non-operating pension and postretirement expenses represent the components of net periodic benefit costs other than service cost. Pension costs allocated to BDS and BGS businesses supporting government customers are computed in accordance with U.S. Government Cost Accounting Standards (CAS), which employ different actuarial assumptions and accounting conventions than GAAP. CAS costs are allocable to government contracts. Other postretirement benefit costs are allocated to all business segments based on CAS, which is generally based on benefits paid. Management uses core operating earnings/(loss), core operating margin and core earnings/(loss) per share for purposes of evaluating and forecasting underlying business performance. Management believes these core measures provide investors additional insights into operational performance as they exclude non-service pension and post-retirement costs, which primarily represent costs driven by market factors and costs not allocable to government contracts. A reconciliation of these non-GAAP measures to the most directly comparable GAAP measure is provided on page 12 and page 13.

Free Cash Flow

Free cash flow is GAAP operating cash flow reduced by capital expenditures for property, plant and equipment. Management believes free cash flow provides investors with an important perspective on the cash available for shareholders, debt repayment, and acquisitions after making the capital investments required to support ongoing business operations and long term value creation. Free cash flow does not represent the residual cash flow available for discretionary expenditures as it excludes certain mandatory expenditures such as repayment of maturing debt. Management uses free cash flow as a measure to assess both business performance and overall liquidity. See Table 2 on page 2 for reconciliation of free cash flow to GAAP operating cash flow.

Caution Concerning Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Words such as “may,” “should,” “expects,” “intends,” “projects,” “plans,” “believes,” “estimates,” “targets,” “anticipates,” and similar expressions generally identify these forward-looking statements. Examples of forward-looking statements include statements relating to our future financial condition and operating results, as well as any other statement that does not directly relate to any historical or current fact. Forward-looking statements are based on expectations and assumptions that we believe to be reasonable when made, but that may not prove to be accurate. These statements are not guarantees and are subject to risks, uncertainties, and changes in circumstances that are difficult to predict. Many factors could cause actual results to differ materially and adversely from these forward-looking statements. Among these factors are risks related to: (1) general conditions in the economy and our industry, including those due to regulatory changes; (2) our reliance on our commercial airline customers; (3) the overall health of our aircraft production system, production quality issues, commercial airplane production rates, our ability to successfully develop and certify new aircraft or new derivative aircraft, and the ability of our aircraft to meet stringent performance and reliability standards; (4) changing budget and appropriation levels and acquisition priorities of the U.S. government, as well as significant delays in U.S. government appropriations; (5) our dependence on our subcontractors and suppliers, as well as the availability of highly skilled labor and raw materials; (6) work stoppages or other labor disruptions; (7) competition within our markets; (8) our non-U.S. operations and sales to non-U.S. customers; (9) changes in accounting estimates; (10) realizing the anticipated benefits of mergers, acquisitions, joint ventures/strategic alliances or divestitures; (11) our dependence on U.S. government contracts; (12) our reliance on fixed-price contracts; (13) our reliance on cost-type contracts; (14) contracts that include in-orbit incentive payments; (15) unauthorized access to our, our customers’ and/or our suppliers’ information and systems; (16) potential business disruptions, including threats to physical security or our information technology systems, extreme weather (including effects of climate change) or other acts of nature, and pandemics or other public health crises; (17) potential adverse developments in new or pending litigation and/or government inquiries or investigations; (18) potential environmental liabilities; (19) effects of climate change and legal, regulatory or market responses to such change; (20) changes in our ability to obtain debt financing on commercially reasonable terms, at competitive rates and in sufficient amounts; (21) substantial pension and other postretirement benefit obligations; (22) the adequacy of our insurance coverage; and (23) customer and aircraft concentration in our customer financing portfolio.

Additional information concerning these and other factors can be found in our filings with the Securities and Exchange Commission, including our most recent Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Any forward-looking statement speaks only as of the date on which it is made, and we assume no obligation to update or revise any forward-looking statement, whether as a result of new information, future events, or otherwise, except as required by law.

The Boeing Company and Subsidiaries

Consolidated Statements of Operations

(Unaudited)

The Boeing Company and Subsidiaries

Consolidated Statements of Financial Position

(Unaudited)

The Boeing Company and Subsidiaries

Consolidated Statements of Cash Flows

(Unaudited)

The Boeing Company and Subsidiaries

Summary of Business Segment Data

(Unaudited)

The Boeing Company and Subsidiaries

Operating and Financial Data

(Unaudited)

The Boeing Company and Subsidiaries

Reconciliation of Non-GAAP Measures

(Unaudited)

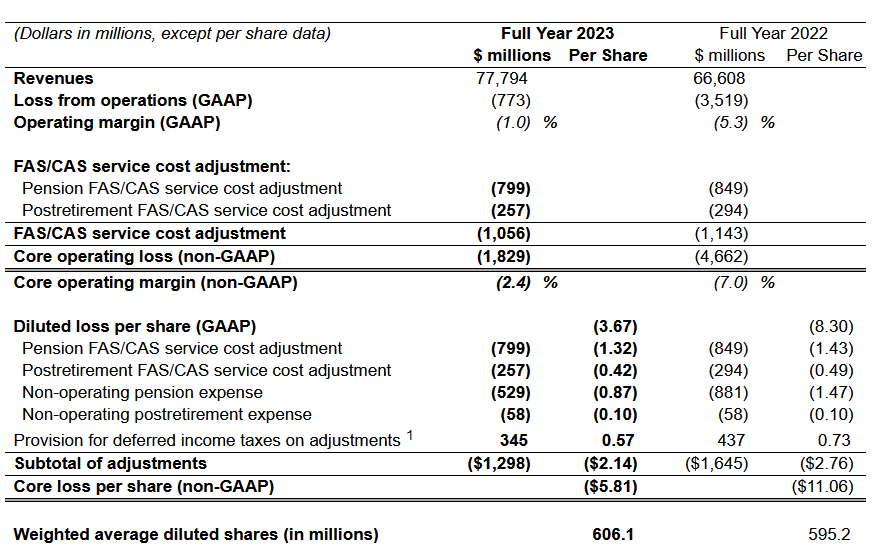

The tables provided below reconcile the non-GAAP financial measures core operating earnings/(loss), core operating margin, and core earnings/(loss) per share with the most directly comparable GAAP financial measures, earnings/(loss) from operations, operating margin, and diluted earnings/(loss) per share. See page 5 of this release for additional information on the use of these non-GAAP financial measures.

The Boeing Company and Subsidiaries

Reconciliation of Non-GAAP Measures

(Unaudited)

The tables provided below reconcile the non-GAAP financial measures core operating earnings/(loss), core operating margin, and core earnings/(loss) per share with the most directly comparable GAAP financial measures, earnings/(loss) from operations, operating margin, and diluted earnings/(loss) per share. See page 5 of this release for additional information on the use of these non-GAAP financial measures.

SOURCE Boeing

Be the first to comment on "Boeing Reports Fourth Quarter Results"